Bitcoin Trends – W1 July 2025

US fiscal hyper-booster: is Bitcoin ready to break through $110K on Short-Squeeze wave and Institutional demand?

TL;DR:

At the macro level, the "One Big Beautiful Bill" fiscal package may provide short-term momentum, however the accompanying $5 trillion increase in national debt intensifies long-term inflationary risks. US equities maintain optimism: S&P 500 and Nasdaq hit new all-time highs, while European markets correct due to tariff uncertainty. In the crypto sphere, the regulatory front remains favorable: SEC gave green light to Grayscale's multi-crypto ETF, while Circle and Ripple apply for banking licenses. Against this backdrop, Bitcoin consolidates near $108K with 30-day momentum rising to +4.2%, open interest growing another 7%, and exchange reserves steadily declining. Key catalysts for the coming days will be the July 9 tariff deadline, FOMC minutes publication and fresh PCE data, which could trigger a surge in market volatility.

Macroeconomics Over the Past Week

Priority: High

"One Big Beautiful Bill" Fiscal Reform

Conclusion: The bill promises the largest tax cut in US history for middle and working class ($10,000 per year per family) while simultaneously raising the debt ceiling by $5 trillion. This will support consumer spending short-term but increase pressure on debt sustainability and may heighten future inflation risks.

ISM PMI Services Sector (June 2025): 50.8

Conclusion: The services sector returned to expansion after May's decline: growth in business activity (54.2), new orders (51.3) and exports (51.1) with moderate reduction in price pressures. However, continued tariff concerns and declining inventory and supplier productivity indicators point to persisting uncertainty.

Non-Farm Payrolls US Employment (June 2025): +147,000

Conclusion: Job growth substantially exceeded forecasts (110,000) and matches the annual average, reflecting labor market resilience. Main driver was the public sector (education) and healthcare, while the federal level continued reductions, signaling mixed employer sentiment.

This is one of the main indicators of labor market health and consequently, the entire economy's health, essentially the main indicator of pressure on Fed monetary policy.

Priority: Moderate

ADP: Private Sector Job Cuts (June 2025): –33,000

Conclusion: First reduction since March 2023, caused by losses in professional/business services and education/healthcare, but supported by gains in manufacturing and leisure, indicating job redistribution within the economy.

ECB Minutes (June 3–5): Eighth Consecutive Rate Cut, July Pause

Conclusion: ECB emphasizes "extremely uncertain" global trade risks and moderate inflation decline, signaling readiness to maintain flexibility and await clearer data before new easing.

Non-Farm Employment Forecast (June 2025): +110,000 (expected)

Conclusion: Projected slowdown to four-month minimum and unemployment rise to 4.3% reflects increasing employer caution due to tariff and trade uncertainty, though fundamental market stability persists.

Despite the unexpectedly strong NFP report and services ISM sector return to growth, the picture remains dual: the private sector (ADP) lost jobs for the first time in two years. Large fiscal stimulus ("One Big Beautiful Bill") promises to fuel consumer demand but simultaneously increases national debt by $5 trillion and intensifies inflationary risks, limiting Fed readiness to quickly ease policy. This signal mix supports short-term appetite for stocks and high-yield bonds but increases probability of volatile pullbacks at any inflation hint.

In the coming week, risk assets will receive positives from fiscal momentum and stable labor market, essentially capable of pushing assets to new highs, while growing debt and tariff concerns will provoke flows into gold, dollar, and short-term Treasuries.

Volatility will intensify around PCE data and Powell's testimony: soft Fed chair tone will confirm the "bullish" scenario, while harsh inflation accents may trigger equity correction.

Stock Market Over the Past Week

Priority: High

European Indices STOXX 50 and STOXX 600 –0.5% Friday and Weekly

Conclusion: Investors returned to tariff concerns ahead of July 9 deadline: new US notifications to trading partners and failed EU negotiations pressure export-oriented sectors, especially raw materials, technology, and automotive.

S&P 500 and Nasdaq 100 Closed at Record Levels Thursday

Conclusion: Optimism around strong NFP (+147,000 June jobs) and trade deal progress (Vietnam, China) allowed S&P 500 and Nasdaq 100 to rise +0.8% and +1.0% Thursday. However, Friday markets were closed for July 4th holiday.

Priority: Moderate

Technology Sector Leads Growth

Conclusion: Nvidia +1.3% and Synopsys +4.2% gained support from lifting some export restrictions on chip design software, continuing to reflect strong AI-segment interest.

Holiday Effect and Shortened Sessions

Conclusion: Friday trading was canceled due to Independence Day, and Thursday saw early close, smoothing volatility and adding a break to weekly dynamics.

Weekly Summary

S&P 500 +0.6%

Nasdaq 100 +0.8%

Dow Jones +0.5%

STOXX 50/600 –0.3%

American indices finished the short trading week with moderate growth thanks to strong employment data and trade deal progress, while European markets were pressured by tariff uncertainty.

Next Week

Trade Deadlines: End of 90-day US tariff suspension (July 9) and possible partner notifications.

FOMC Minutes: Search for signals on further monetary policy - markets await Fed details.

Data Calendar:

US: Light calendar (PCE, industrial goods orders, trade balance).

China: CPI, PPI and foreign trade.

Europe: UK GDP, German industrial production and trade balance.

Canada: Employment report.

Important News of the Past Week

Priority: High

SEC Approves Grayscale Crypto ETF (BTC, ETH, XRP, SOL, ADA), opening path for new products under relaxed listing rules.

Circle Applies for US Digital Bank Charter to manage USDC reserves under federal oversight within framework of upcoming stablecoin laws.

Ripple Requests US National Banking License and Fed Account to boost RLUSD stablecoin and expand crypto services under Fed control.

Robinhood Launches Tokenized US Stocks, Crypto Wallets and Staking in EU and US and announces proprietary L2 blockchain based on Arbitrum.

Turkey Blocks PancakeSwap and 45 More Crypto Sites for providing unauthorized services under new regulations.

MicroStrategy Buys Additional 4,980 BTC for $531.9M, bringing reserves to 597,325 BTC (≈3% of total supply).

Priority: Moderate

Ondo Finance to Acquire SEC-Regulated Broker Oasis Pro to expand tokenized securities market, focusing on US stocks for global clients.

Pomerantz Law Firm Files Class Action Against MicroStrategy, accusing company of misleading BTC investment disclosures and new reporting standard violations.

New York Judge Allows Celsius to Continue $4.3B Lawsuit Against Tether regarding alleged premature BTC liquidation before mandatory waiting period completion.

AllUnity (DWS, Galaxy, Flow Traders) Receives BaFin Approval for EURAU - Germany's first euro stablecoin under MiCA standards.

Abu Dhabi to Issue First Tokenized Bonds on FAB and HSBC Orion Platforms, advancing national real asset tokenization strategy.

Bit Digital Raises $163M from Share Placement to expand ETH treasury, winding down Bitcoin mining in favor of Ether accumulation.

American Bitcoin Receives $220M, Including $10M in BTC, to expand mining capacity and replenish treasury ahead of SPAC public listing.

Circle Launches Gateway for USDC Access via Avalanche, Base and Ethereum, providing real-time cross-chain liquidity.

Analyst Sani Detected Movement of 80,000 BTC Likely Belonging to Roger Ver, after six addresses with total balance of 60,000 BTC and two more previously marked as "Individual X" activated after 14 years of inactivity.

Priority: Low

FTX Recovery Trust Risks Losing Payout Ability in China and Russia, if local regulators prohibit such distributions.

Riot Platforms Mined 450 BTC in June (~$49.3M) — 76% growth compared to last year.

Conclusions

This week's key focus is on expanding institutional infrastructure and easing regulatory barriers. Grayscale ETF approval and Circle and Ripple steps toward banking licenses create foundation for crypto asset integration into traditional finance. Large buyers MicroStrategy and American Bitcoin continue building BTC reserves, while Ondo Finance and Abu Dhabi move the tokenized securities market forward.

Simultaneously, new legal proceedings (Pomerantz vs MicroStrategy, Celsius vs Tether) and site blockings in Turkey remind of persisting legal and regulatory risks.

Bitcoin Trading Week Macro Analysis

1. BTC/USD Pair Analysis

Key Weekly Indicators

Current Price: ≈ $108K

Local High: $110.5K

Local Low: $105.1K

Trend

This week BTC first bounced from $105K level on rising volumes, then rebounded and reached $110.5K peak. The second half of the period passed in range tightening around $108K with gradual volume decline, indicating profit-taking and position accumulation before new momentum.

Conclusions

Key Resistance: $110.5K – confident breakout on elevated volumes could open path to $115–$120K.

Local Support: $108K – holding this level will preserve bullish momentum and reduce pullback risk.

Strong Base Support: $105K – critical zone for assessing correction depth and reassessing long-term positions.

2. Bitcoin Price Momentum (30-day)

Weekly Analysis

This week Bitcoin's 30-day momentum continued recovery from neutral zone and currently consolidated at +4.2%. After brief stagnation we observe gradual momentum growth.

Conclusions

Momentum above zero (+4.2%) confirms weakening bearish pressure and indicates resuming bullish activity.

Momentum level still significantly below long-term average (+10%), indicating insufficient new buying volume for larger price advance.

3. Options Analysis

Market Structure

Call Options Dominance:

Green bars concentrated on $110,000–$130,000 strikes, with peak volumes:$130,000 (≈ 9M)

$127,500 (≈ 8M)

$125,000 (≈ 6M)

$122,500 (≈ 5M)

$120,000 (≈ 4M)

This indicates active hedging for growth above current Max Pain level ($108,000).

Put Options:

Red bars dominate $85,000–$100,000 strikes, with maximums:$85,000 (≈ 10M)

$87,500 (≈ 7.5M)

$90,000 (≈ 6M)

$92,500 (≈ 5M)

$95,000 (≈ 4.5M) Above $100,000 Put volumes quickly decline:

$102,500 (≈ 2.5M)

$105,000 (≈ 2M)

$107,500 (≈ 1M)

Comparative Analysis with Previous Week

Max Pain Change: Max Pain level rose from $107,000 to $108,000, reflecting further shift in options player interest balance toward higher prices.

Volume Dynamics:

Calls: volumes on $125,000–$130,000 strikes increased about 1–2M, mid-range ($120,000–$122,500) remained at previous level (≈ 4–5M).

Puts: volumes on key $85,000–$90,000 strikes decreased ~1–2M, while $92,500–$100,000 zone dropped ~0.5–1M.

Forecast

Possible Growth:

Holding $108,000 support and further Call volume increases could lead to testing $110,000–$112,500 zone, and with confident breakout - to $120,000.Correction Risks:

Breaking $108,000 level with simultaneous Put volume growth could return price to $105,000–$106,500 range, where main "bear" protection is concentrated.

Bitcoin Network Data Analysis This Week

1. Transfer Volume (7d):

Previous Week: 4,080,842 BTC

This Week: 3,117,333 BTC

Change: 🔴 −23.70%

Comment: Another weekly decline in transfer volumes (−23.7%) reflects on-chain activity lull phase: users less frequently move large amounts, awaiting further market signals.

2. Network Hashrate:

Previous Week: 911,172,262,801 EH/s

This Week: 912,804,149,373 EH/s

Change: 🟢 +0.18%

Comment: Slight hashrate growth (+0.2%) indicates stable return of computing power to network after previous technical pauses.

3. Number of Active Wallets (7d):

Previous Week: 8,084,077

This Week: 7,613,316

Change: 🔴 −5.82%

Comment: Nearly 6% reduction in active addresses indicates continuing consolidation and decreased retail transactional activity.

4. Market Capitalization:

Previous Week: $2,134,657,250,024

This Week: $2,152,333,457,956

Change: 🟢 +0.83%

Comment: Capitalization growth (+0.8%) reflects moderate new money inflow to Bitcoin amid declining transactional activity.

5. Market Price:

Previous Week: $107,664

This Week: $108,167

Change: 🟢 +0.47%

Comment: Price grew 0.5% weekly while on-chain metrics consolidated.

6. BTC Exchange Reserves:

Previous Week: 2,430,205 BTC

This Week: 2,409,499 BTC

Change: 🔴 −0.85%

Comment: Continuing exchange outflow (−0.85%) strengthens long-term accumulation and reduces liquid reserve volume.

Conclusions

Waiting Phase: Sharp transfer volume drop (−23.7%) and active wallet decrease (−5.8%) indicate market's wait-and-see position.

Network Stability: Small hashrate growth (+0.2%) emphasizes network reliability even during current consolidation.

Moderate Capitalization and Price Growth: +0.8% to capitalization and +0.5% to price reflect cautious investor optimism.

Long-term Accumulation: Exchange outflow (−0.85%) continues strengthening foundation for next growth phase when demand drivers appear.

On-Chain Metrics

Bitcoin Growth Rate (Market Cap vs. Realized Cap) 365DMA

Over the past quarter we observed recovery of annual Growth Rate (difference between market and realized capitalization) from negative to positive zone. In mid-June the 365-day moving average growth was at 0.00056, and by early July rose to 0.00083. This means the market cap premium over realized cap is gradually expanding – a sign of strengthening long-term bullish fundamentals and accumulation as new price rally approaches.

This week the Growth Rate indicator demonstrated high volatility:

July 2 spike to +0.0288 (one-day growth over 2.8%) reflected heightened buyer activity.

July 4 pullback to –0.0241 profit-taking and capital rotation.

July 5 moderate recovery to +0.00158 indicates resumed supply-demand balance, but with more measured participant sentiment. Meanwhile market cap holds in $2.10–2.18 trillion range, indicating consolidation at historical highs.

Conclusions.

365-day SMA growth above zero and its steady upward slope confirm favorable background formation for further BTC growth.

Short-term volatility is normal market reaction, but maintaining growth above zero line indicates demand prevalence.

Bitcoin Futures

Aggregated Open Interest in Bitcoin Futures (% Change)

Over the past week, aggregated open interest in BTC futures in 30-day change terms grew +7%. This is the first sustained rise after prolonged position outflow in May-June, when 30D % Change dropped to –12% zone. Now we observe renewed trader interest: both net contract volume and leverage appetite are growing.

Increasing open interest means market participants are actively building new positions – a typical sign of resuming upward dynamics. When OI grows alongside price, it indicates bulls are ready to back movement with fresh money.

Nevertheless, to confirm new rally we need to monitor OI growth staying above +10% level and accompanied by trading volume increases. If open interest continues gaining momentum, this will create additional impulse for continued BTC growth.

Bitcoin Futures Open Interest NET Position

Let's drop to lower timeframe and check net position status in futures market. On hourly chart, net futures position (OI Net Position) returned to positive zone: net "bullish" open position volume stands at +26 million USD. After brief flat and bearish sentiment early this week, we see steady long building: average net position line has been rising above zero for over 12 consecutive hours.

Net position recovery indicates market participants again show readiness to take long positions despite relative price stagnation around $108,000.

Bitcoin Futures Long Short Liquidations Dominance

Over the past week, Futures Long Short Liquidations Dominance metric dropped to –9.5% level, meaning approximately 9.5% more short positions were liquidated than longs. This is a classic short squeeze sign: weak shorts are forced to close, pushing price up through stop hunting. Meanwhile liquidated short volume doesn't exceed extreme levels of past rallies, but sentiment favoring short liquidations is already evident.

Breaking nearest $110K resistance could trigger new short liquidation wave and accelerate price toward next targets.

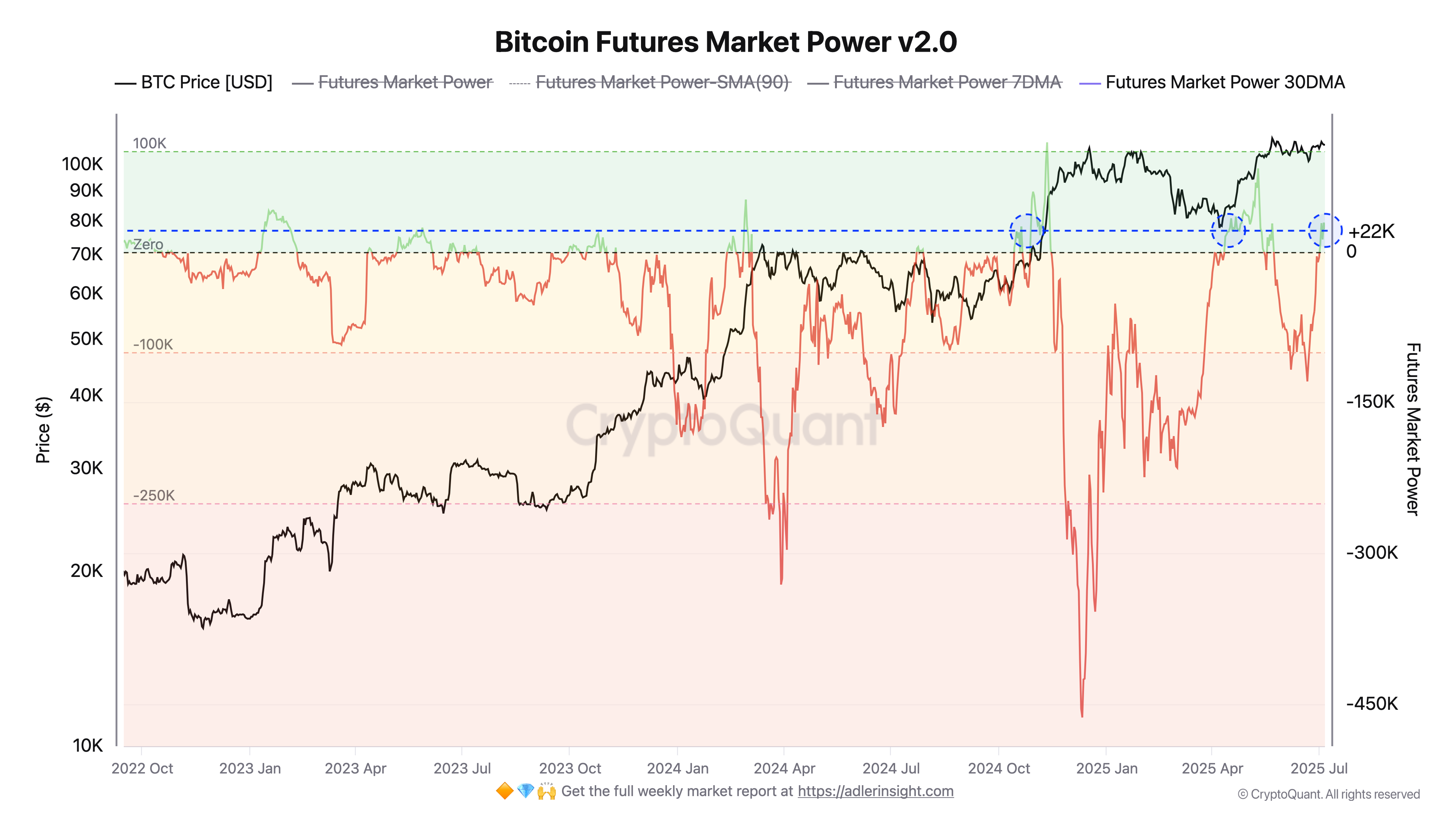

Bitcoin Futures Market Power v2.0

Bitcoin Futures Market Power - this indicator combines open interest dynamics, funding rate and taker order activity. When it goes above zero (30-day SMA currently +22,000), it means long positions in futures are growing in volume, and taker buyers dominate sellers. Simply put, bullish consensus is forming in the market.

Current levels are still far from past rally extremes (where Market Power rose to +80 – +100K). This indicates that while bulls regained initiative, full "overheating" and bullish euphoria aren't present yet.

Conclusion.

Thanks to US fiscal "mega-booster" and unexpectedly strong NFP, global risk appetite will receive short-term doping, but July 9 tariff deadline and fresh PCE data will quickly return conversation to inflation and debt burden. This creates ground for sharp single-day movements in both stocks and crypto assets.

On Bitcoin's side, picture is "compressed spring": open interest growth (+7% 30D) and net long in OI Net Position with moderate price growth and falling network activity indicates capital is carefully accumulating, awaiting signals. Breaking $110.5K could trigger chain short liquidation and accelerate march to $115-120K, while failing below $108K opens road to $105K and tests recent buyer strength.

Key triggers for coming days are Powell's tone in FOMC minutes and tariff negotiation outcome. Soft regulator + no tariff escalation will confirm bullish scenario; harsh statements or new duties will return volatility and strengthen defensive asset demand.

Next Week Forecast

Investment Recommendations: 🟢 OUTPERFORM (Accumulate)

More details about the rating can be found at this link: https://adlerinsight.com/Adler_Insight_Rating.pdf

Good luck in the upcoming trading week!

AAJ

Disclaimer:

This material has been prepared solely for informational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities, digital assets, or other financial instruments. The information presented in this report is considered reliable; however, its accuracy or completeness is not guaranteed. Past performance is not indicative of future results. Any investment decisions are made by the investor independently, taking into account personal financial circumstances and, if necessary, after consultation with a qualified professional. The author and affiliated parties may hold positions in the assets mentioned in this report. The author and publisher accept no responsibility for any direct or indirect losses arising from the use of this information.

Risks:

High volatility may lead to sharp fluctuations in value, adversely affecting investors' portfolios. Significant price swings may reduce the attractiveness of BTC to institutional investors, especially in the derivatives segment (futures, options). Potential tightening of regulatory requirements by governments and central banks may restrict access to BTC markets and reduce liquidity. Issues with custodial services, centralized exchanges, and hacking incidents could undermine confidence in the asset and negatively impact liquidity.

Such a pleasure to go through your detailed analysis! Thx Axel!