Weekly Engine #95

W2 May 2026

GM/GN.

In the middle of the week, James Van Straten from CoinDesk wrote to me on X:

You’ve been bearish the whole way up lol.

And here I have to admit it: lately, I really have been too aggressive toward the bullish scenario. So it is worth explaining my position more precisely.

After Bitcoin fell from $125K to $60K, the market has been trying to recover. And if you look at the terminal, the AI periodically reminds you of this. But a recovery is not yet a confirmed new bull cycle. Many on-chain metrics have not yet reached the zones that corresponded to a full market bottom. Let’s dig into the data.

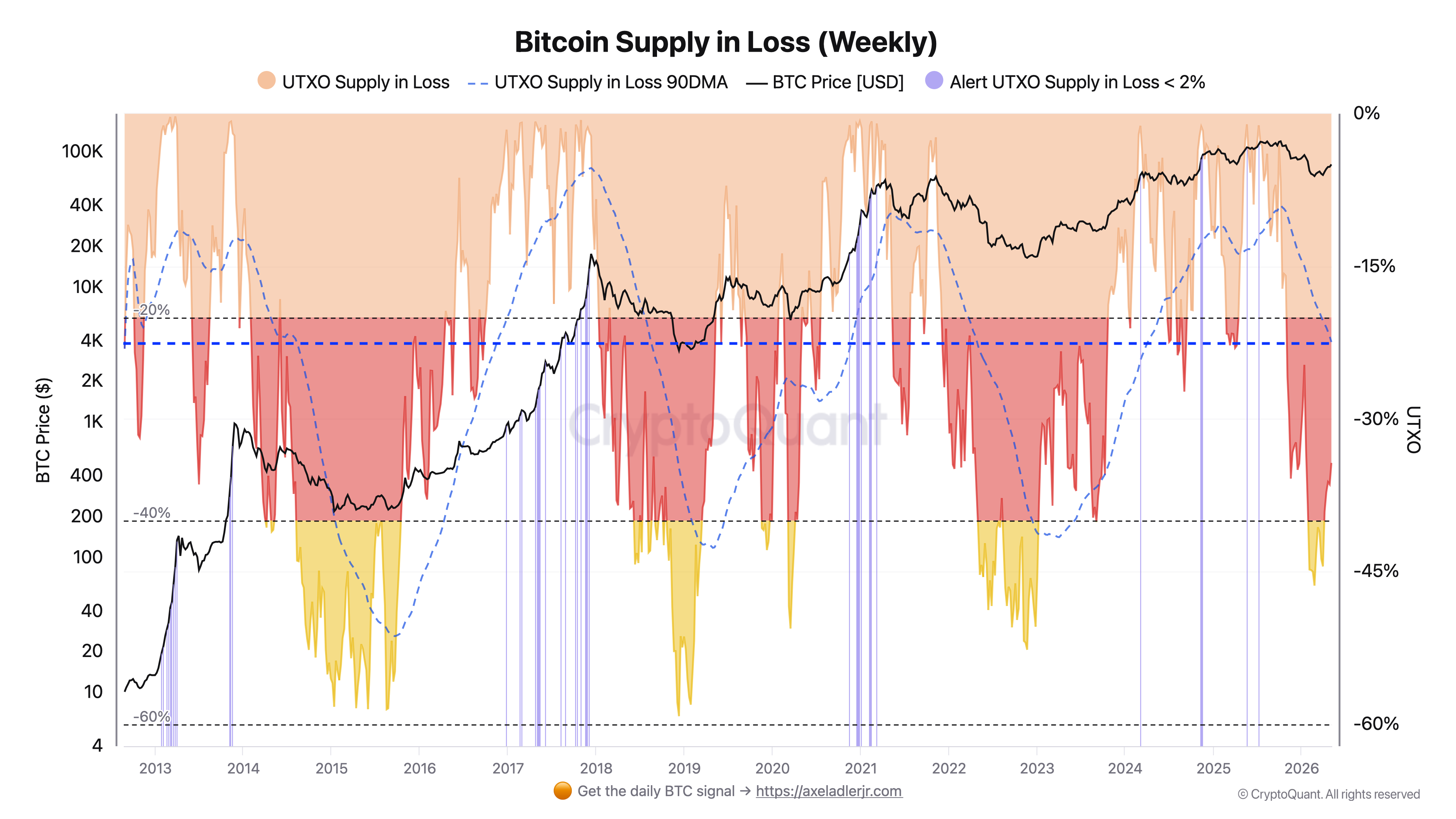

Look at the weekly Bitcoin Supply in Loss chart, especially the quarterly UTXO Supply in Loss 90DMA metric. Am I really the only one seeing this pattern?

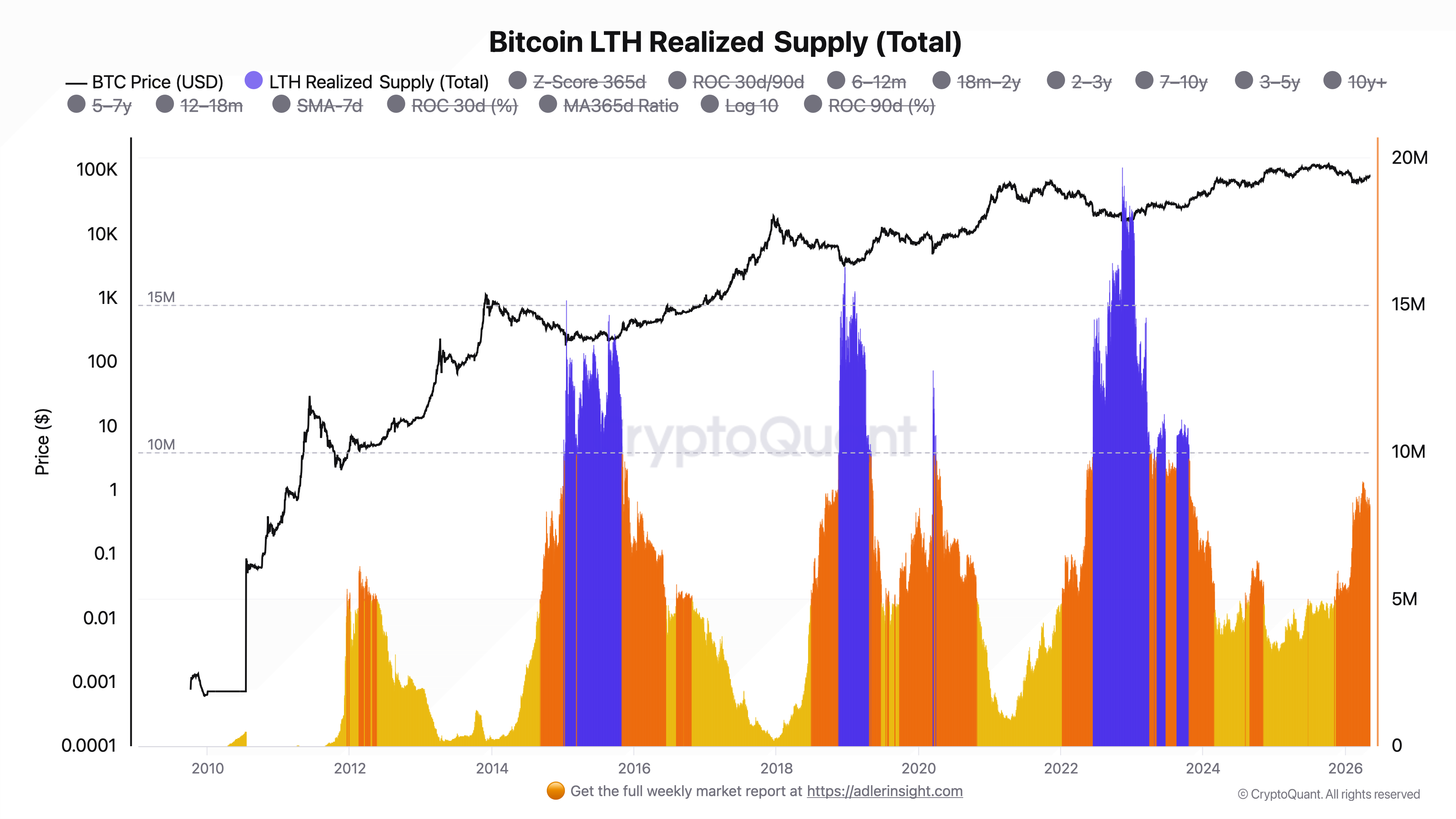

Bitcoin LTH Realized Supply shows that long-term holders have not yet reached the accumulation structure that usually appears closer to the end of a bear cycle. We need more time before we see the blue bars.

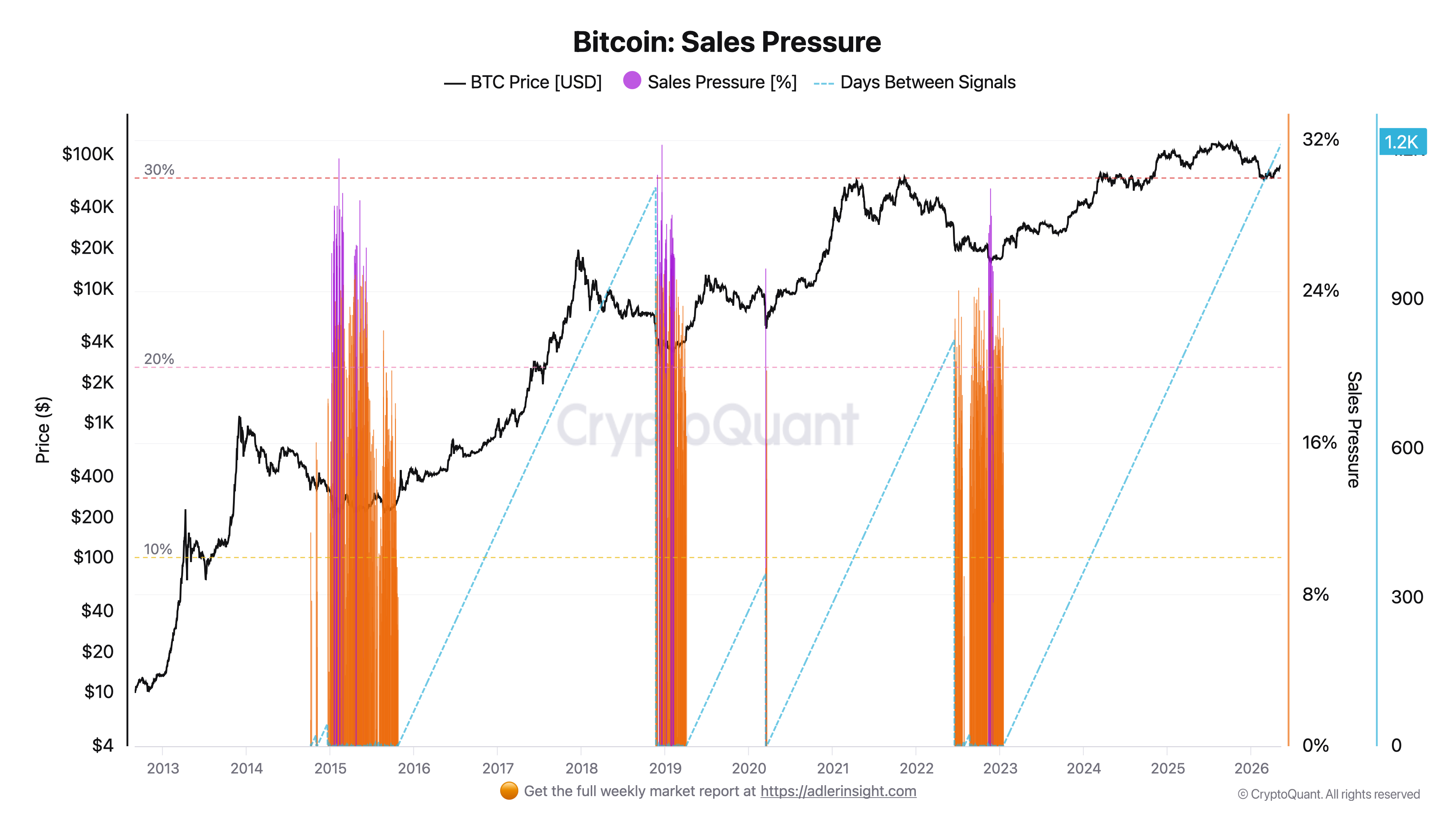

Have we seen real spot selling pressure in this cycle? Also no. Bitcoin: Sales Pressure confirms that the market has not yet gone through a full phase of spot capitulation. There has not been real stress in the market yet.

I could continue, but the idea is clear. My position remains the same: the current move higher is a recovery after a sharp decline, not a confirmed start of a new bull cycle, which several major KOLs claimed last week.

For me to change my view, I need to see not just price growth, but confirmation from the on-chain structure, sustainable spot demand, and the removal of key supply-side pressure risks. Until then, I remain cautious. Not because I want to be bearish, but because the structure of the Bitcoin market does not yet provide strong enough confirmation of the opposite.

The on-chain data is clear, so let’s look at the broader narrative.

Deloitte’s Financial Well-Being Index fell back to 101 points in March. The reason is rising anxiety about the future and higher inflation expectations.

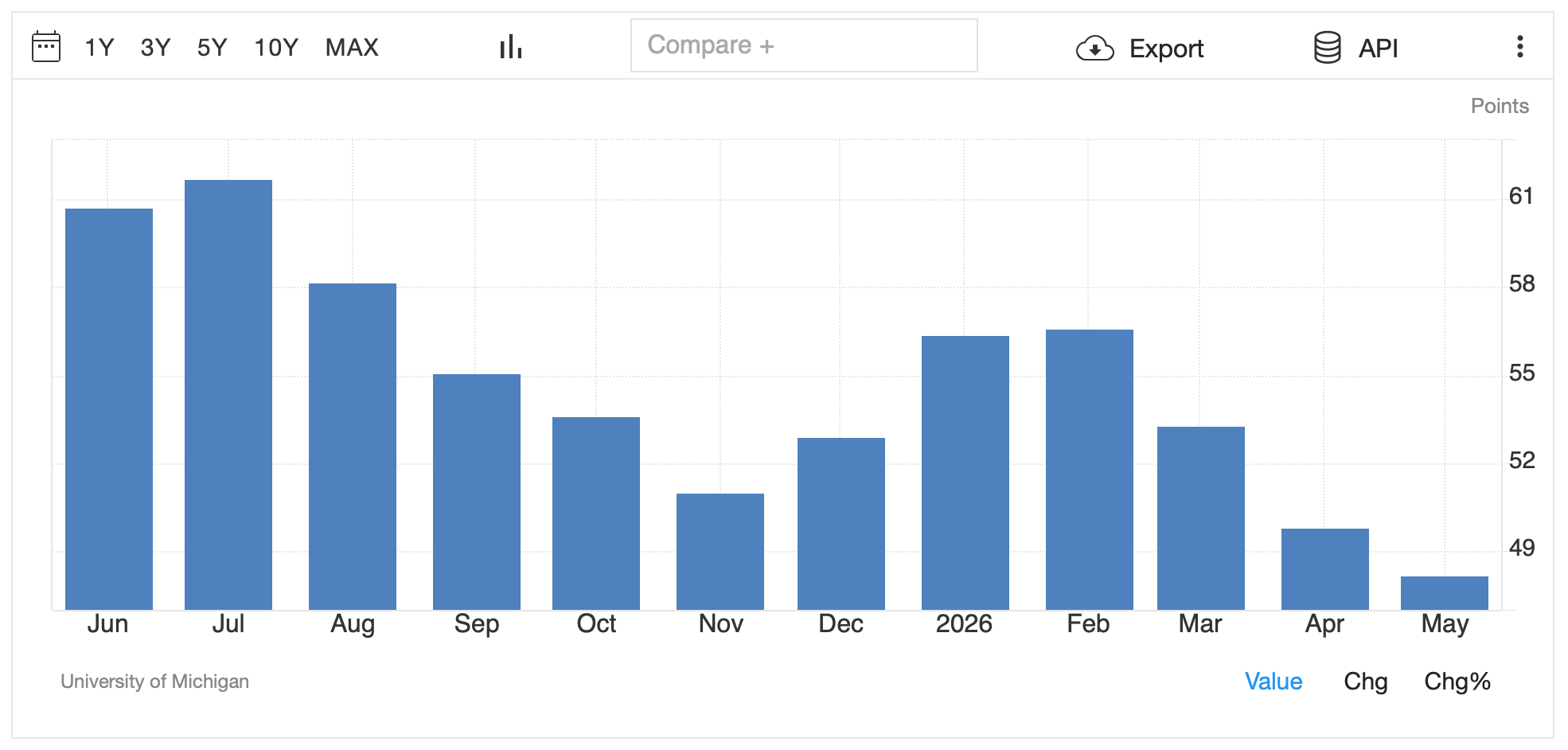

The University of Michigan Consumer Sentiment Index fell to a record low of 48.2 in early May 2026.

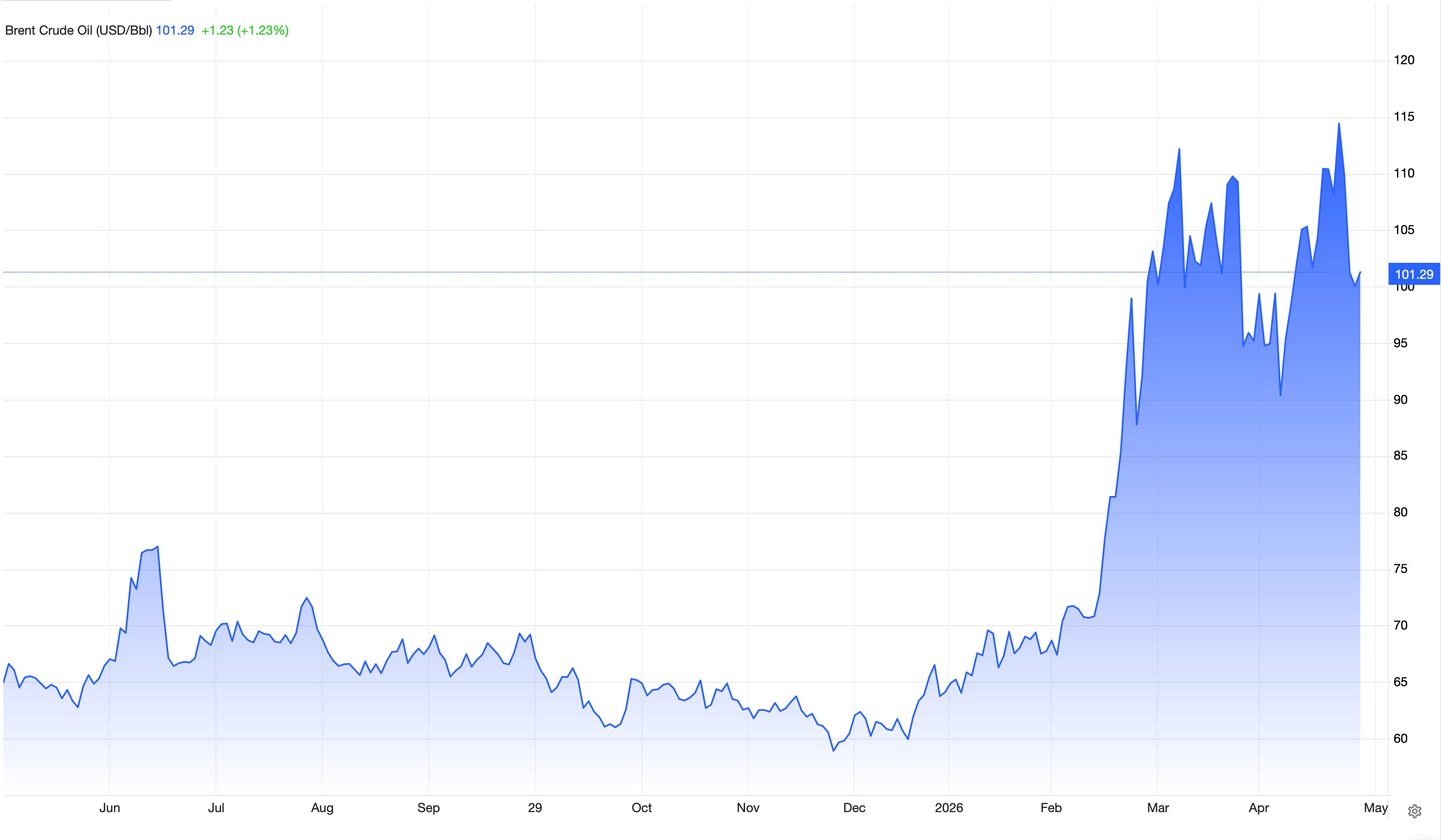

Brent crude futures are holding near $100 per barrel after renewed clashes between the United States and Iran. This is increasing doubts about the durability of the fragile ceasefire and has cooled hopes for a quick peace agreement. For the global economy, oil closer to $70 per barrel would be more comfortable: anything above $100 starts to intensify inflationary pressure and weighs on consumers, transportation, production, and business margins.

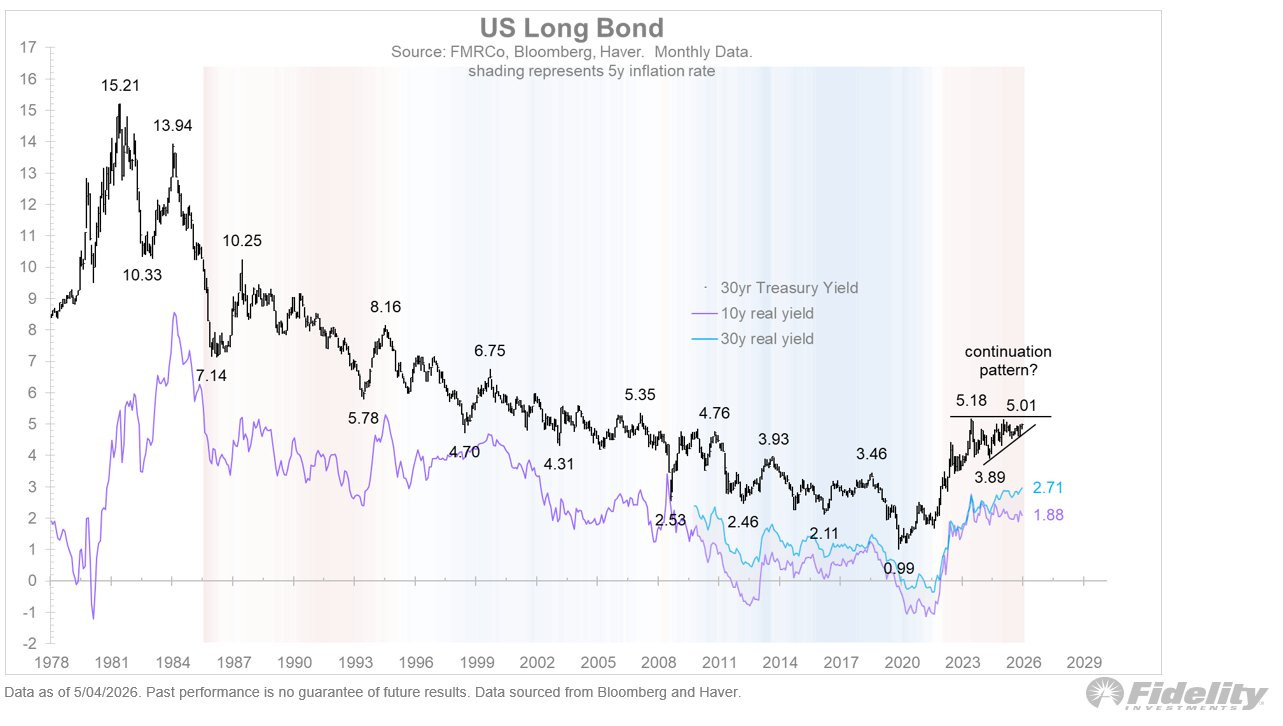

Jurrien Timmer (Dir. of Global Macro Fidelity) writes: "All this may be happening when the long bond is coiling inside what looks like a bearish continuation pattern. Real rates are rising, as are inflation expectations via the TIPS market. Remember: nothing good happens above 4.5% (for the 10-year)." The bond market is signaling that rates will stay high longer than the market would like. This creates pressure for stocks, real estate, lending, and the economy as a whole. The rule is very simple: high interest rates put pressure on assets.

Jerome Powell’s term as Fed Chair expires on May 15. From that date, Kevin Warsh could take over as Fed Chair if his nomination is approved by the full Senate. The Senate Banking Committee has already approved his nomination in a party-line vote: 13 Republicans in favor, 11 Democrats against. Formally, Warsh has not been confirmed yet, but the process is moving forward, and May 15 remains the key date for a change in Fed leadership.

But the main question is not Warsh’s candidacy itself, but the fact that the market is no longer pricing in a scenario of quick rate cuts. According to Bloomberg, the swaps market now sees a probability above 50% that the Fed’s next meaningful move could be a rate hike, not a cut. In other words, traders are not hedging quick cuts, but the risk that the new Fed will be forced to keep rates high or even raise them. This is a strong shift from the March consensus among economists, where a Bloomberg survey still expected two rate cuts in 2026 of roughly 50 bps, with the first cut in June.

CME FedWatch confirms the cautious picture: for the next meeting on June 17, 2026, the market is almost fully pricing in no change in rates, rather than a cut.

The takeaway is simple: even if Warsh is politically perceived as a more dovish candidate, the rates market is saying something else right now. With oil at $100, rising inflation expectations, and the 10-year Treasury yield above 4.5%, it will be difficult for the Fed to quickly move toward easing.

I hope I have clarified my market position.

Let’s move on to product news. This week there was another terminal update, thank you for sending feedback, but the main news is elsewhere.

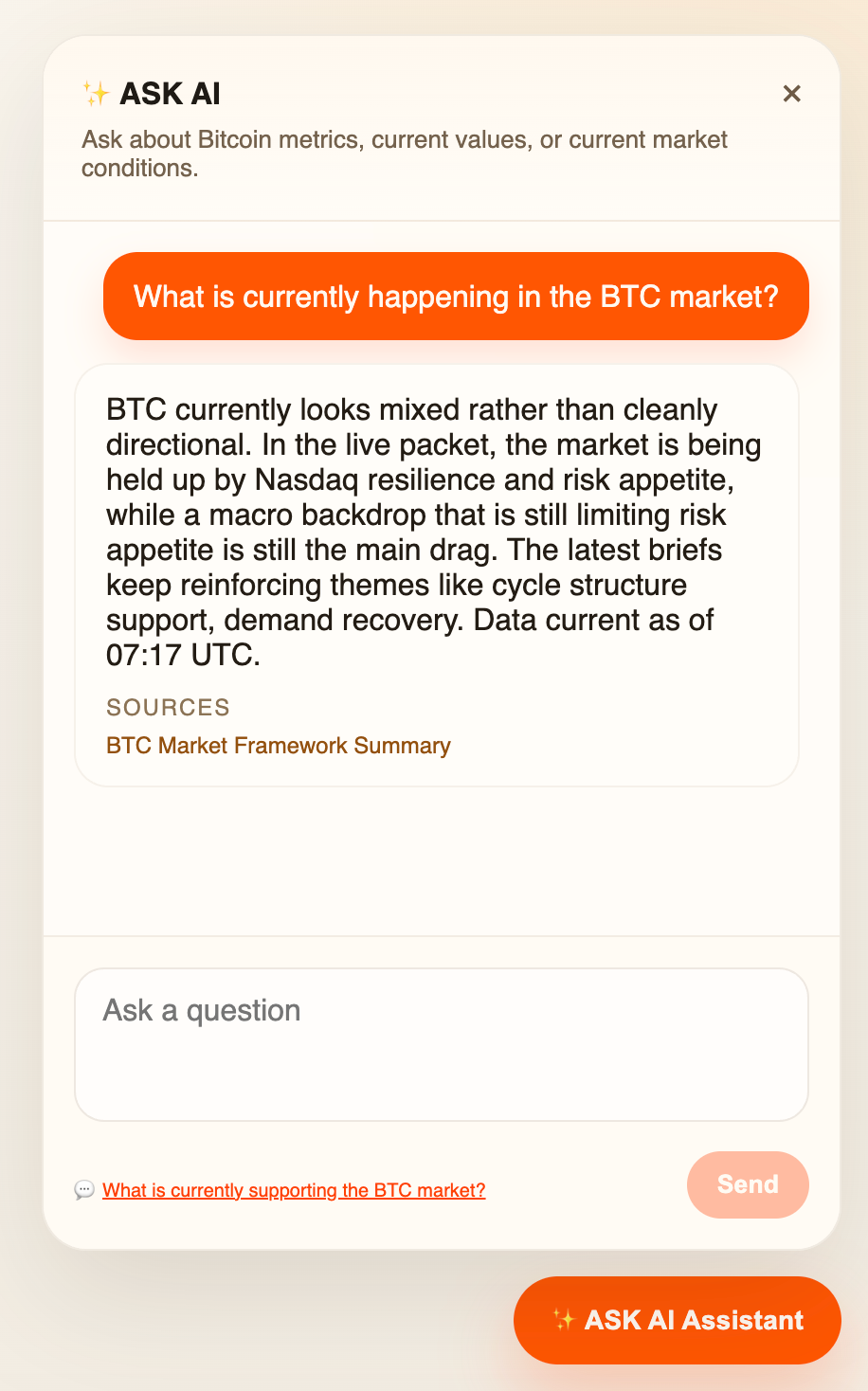

We are finishing development of the ASK AI widget - an intelligent assistant trained on a layer of on-chain and market data. Next week, we plan to launch it on my personal website and begin the process of further training it on your real queries.

After this stage is complete, the Pro version of ASK AI will appear in the terminal without the limitations that will apply to the free version. The assistant will get access to my research, Weekly Engine data, all terminal data, and AI conclusions.

But most importantly - the market-cycle limitation that currently exists in Weekly Engine will be removed.

This means ASK AI will become an independent analytical expert built on top of all the data layers we collect and analyze.

I am really looking forward to this launch myself, because I am extremely interested to see how a modern LLM model will interpret the market when it has access not to noise, but to the right data.

Nevertheless, the main weekly verdict on the market still comes from Weekly Engine. Only a comprehensive weekly analysis of the entire market can produce a clear conclusion. And this is the main question right now: is this already a confirmed market recovery - or just a strong rebound inside an unfinished bearish structure?

In the new issue, we break down what changed across layers L1-L7 compared with last week: where the market really became stronger, what continues to weigh on the structure, where new constraints appeared, and which factors supported this week’s mini-rally.

Keep reading with a 7-day free trial

Subscribe to Adler Insight 💎 Premium to keep reading this post and get 7 days of free access to the full post archives.